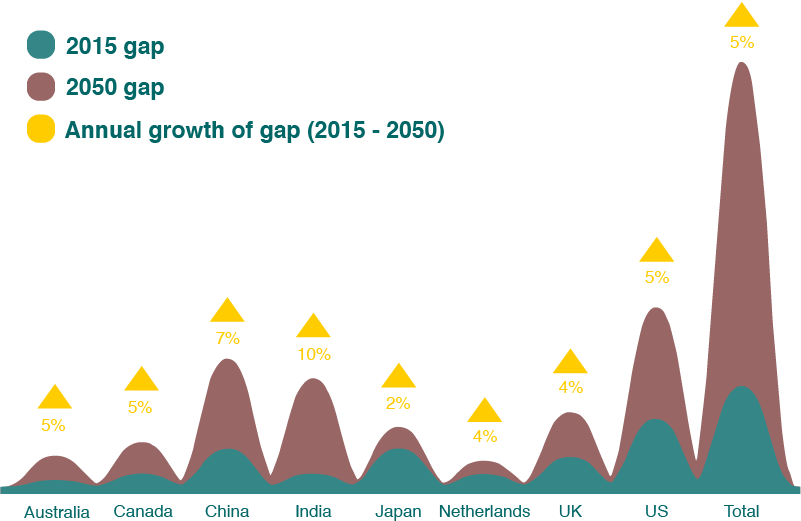

The World Economic Forum has calculated that pension systems across the United States, the United Kingdom, Japan, the Netherlands, Canada and Australia will have a joint shortfall of $224 trillion by 2050. If you add China and India to the equation, the combined gap nearly doubles to $400 trillion. That’s five times the size of the current global economic output. Such a shortfall places severe risks on the incomes and quality of life of future generations while setting the industrialized world up for one of the most widespread pension crises in history.

The Global Pension Crisis

Source: Mercer (2017)

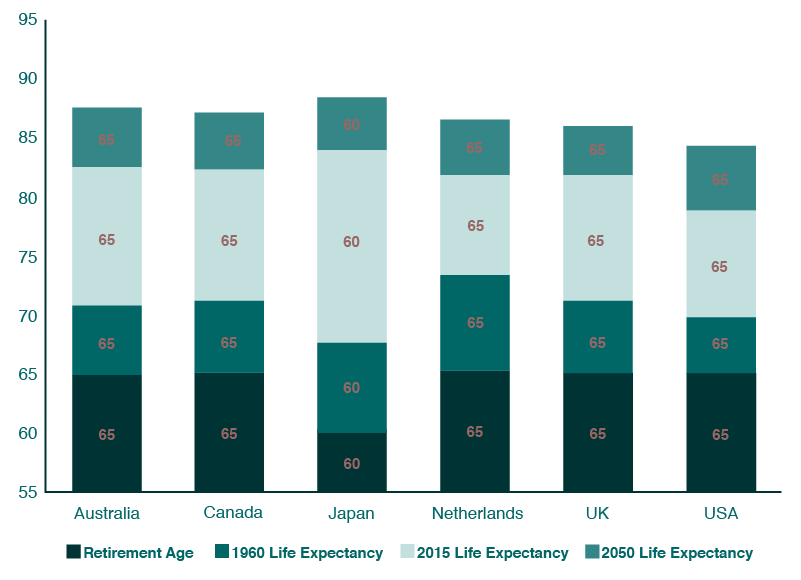

Funding this shortfall will not be easy with global debt levels rising to more than 325% of GDP in 2017, reaching an eye-watering $217 trillion. There is also significant time pressure as the global population already lives much longer than what pension systems were originally designed for. Retirement age for most countries around the world is 65 and yet average lifespans reached 71 years old back in 2015. The global population that has reached retirement age will increase from 600 million today to 2.1 billion by 2050. Average lifespan has been increasing by one year, every five years, with every single person born from now on expected to live for a full century.

Expected Increase in Life Expectancy by 2050

Source: World Economic Forum (2017)

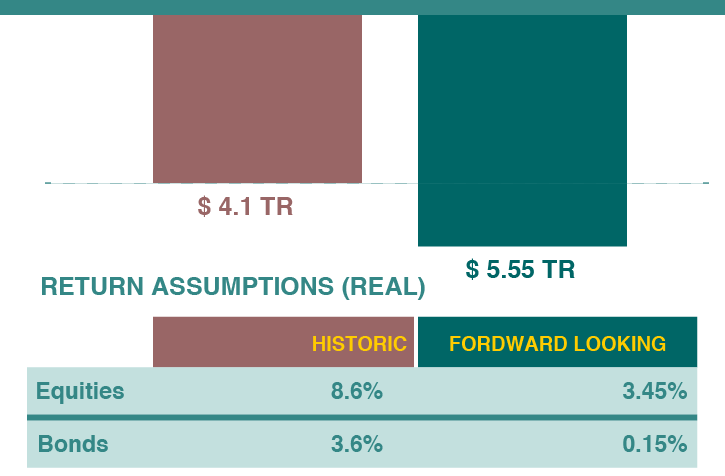

Saving will become increasingly challenging as governments around the world resort to increasing taxes and keeping interest rates low to fund the shortfall. Interest rates have hovered around 0.25% across many of the world’s developed economies for the past five years. Earning 5% on $500,000 yields $25,000, and with interest rates at 0.25%, income drops to $1,250. In real terms, those fractional earnings will disappear, eaten away by the higher inflationary pressure of 2.1% – the average level of inflation in the United States in 2016. At the same time, investment returns for traditional asset classes over the past decade have been comparatively low. Equities have performed up to 5% below historic averages and bond returns have been 3% lower as assets respond to a low interest and inflation rate economic landscape.

Retirement Savings Shortfall in the United States

Source: EBRD (2017)

This new normal of low returns for traditional asset classes has caused investors to diversify away from equity and fixed-income products and opt for an alternative, tangible and risk-adjusted assets. By 2030, allocations to physical assets among institutional investors will reach up to 30% of total portfolio value. Why? Long-lived physical assets that generate stable cash flow streams provide enhanced yields and offer attractive risk-adjusted returns.

Agriculture as an alternative asset provides the necessary services to support a thriving economy and ensure global health. The fundamental drivers will always remain – an expanding global population and a limited supply of the world’s most fundamental resources. The Food and Agriculture Organization (FAO) have calculated that a 70% expansion in global food production will be needed by 2050 to the rising demand of our growing and aging populations. This is expected to cause 60% price increase over the same period in food commodity staples. Farmland prices have already shown impressive performance. Savills Global Farmland Index has increased by 13% each year since 2002 and 7.5% over the past decade.

With longer lifespans, heavy debt, difficult saving conditions and lower investment returns for traditional asset classes, governments around the world will fill the pension-funding shortfall through taxation and low-interest rates. With the global economic environment showing no signs of change, investors will increase exposure to alternative assets such as agriculture in order to secure earnings and build sustainable wealth.