With the Chinese economy growing at its slowest pace for a quarter-century, a wholesale correction in commodity prices since 2011 and the Federal Reserve gradually increasing interest rates, currency devaluation is becoming a trend across emerging markets. Brazil, one of the largest and most significant of these, has shown no exception.

Over the course of 2015, the Brazilian Real fell to its lowest level since its introduction two decades ago at R$4.06 per US$. The Real slid after equities in China, Brazil’s top trading partner, fell into a bear market and prompted a selloff in the raw materials and currencies of commodity-exporting nations. The significant drop in commodities’ pricing, ranging from iron ore (13.5% of Brazil’s total exports), soybeans (9.3% of exports) and crude (5.3%) further pressured the country’s trade balance and sentiment towards the Real softened accordingly.

The Strength of the Brazilian Real Drops Alongside Commodity Prices

% Change in Soybean price (Blue), Brent Crude Oil price (Red) and Brazilian Real/US$ Exchange Rate (Orange)

Source: Bloomberg (2016)

These external factors were compounded by domestic concerns of a political stalemate in Brazil and a corruption investigation at the state-controlled oil company Petrobras. This undermined the value of the Bovespa, which has now reached its lowest level since March 2009. More positively, the electorate has become more demanding and steadfast in their refusal to accept any more corrupt antics from the country’s politicians and captains of industry – a fundamental accomplishment and structural adjustment that can only help underpin and strengthen the economy.

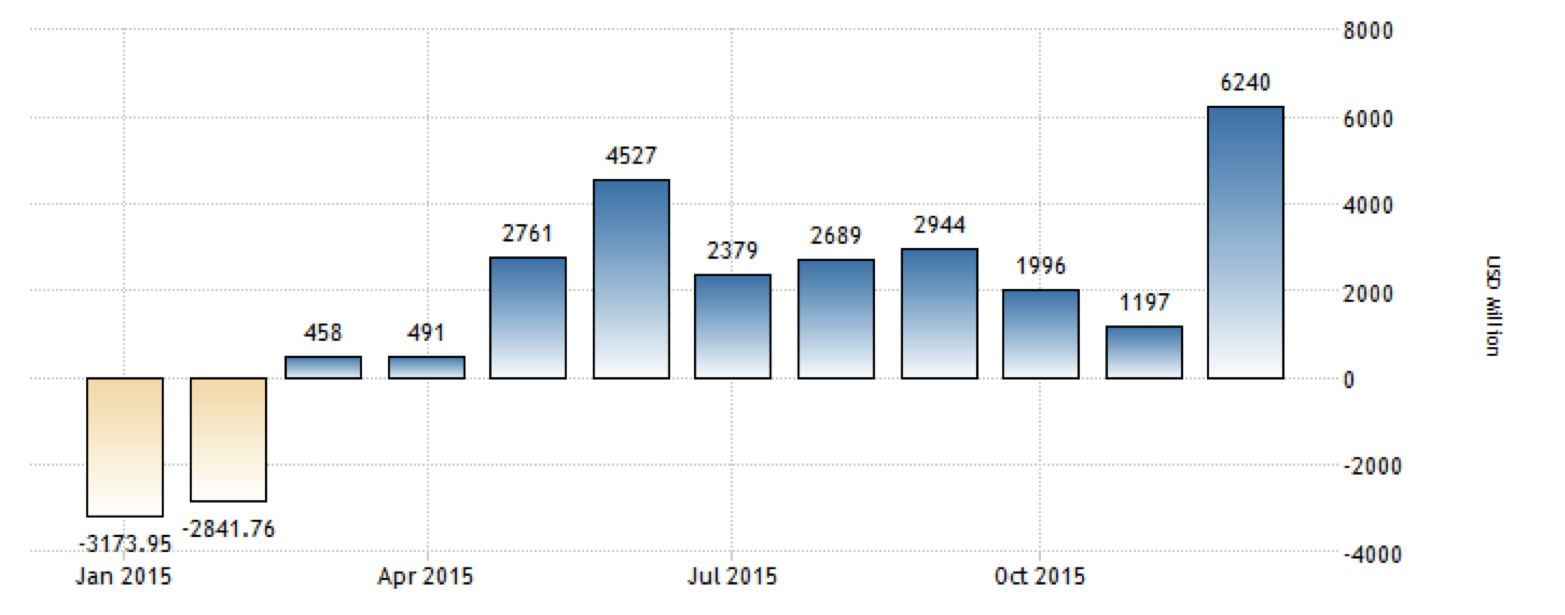

One of the main reasons for a currency to devalue is to retain its competitiveness. If the Real had maintained its value during this unsustainable drop in commodities’ pricing, imports would have remained stable and a significant trade deficit would emerge. When the Real dropped, imports fell while exports stabilized. Brazil rebounded from a deficit of $4 billion in 2014 to a trade surplus of $19 billion last year. This is an indication that the Real’s devaluation is enough to face the drop in commodity prices and that Brazil’s competitiveness is being reestablished.

Brazil Achieved a $19 billion Trade Surplus in 2015

Brazil’s Balance of Trade (US$ Millions)

Source: Trading Economics (2016)

As Brazil’s leading market for exports, China’s financial stability plays a very important role in the Latin American country’s economic future. The recent move from China’s Central Bank to impose strict reserve-requirement ratios on Yuan deposited in the country from overseas financial institutions is a good sign for Brazil. This intervention will help stabilize the Yuan despite recent turmoil in the country’s stock markets. As China is the biggest market for Brazilian exports, a stronger currency will help Brazil’s terms of trade. Essentially, a stronger China equates to a stronger Brazil.

By investing in Brazil when the currency is low, one is effectively buying into undervalued market. With a population disappointed by the empty promises of a leftist party, a more centered government is emerging. Finance Minister Nelson Barbosa has reaffirmed the Brazilian government’s commitment to strict fiscal targets necessary for economic growth. By the time Brazilian President Rousseff leaves office, investor sentiment and appetite for Brazilian assets will have built up to reflect the country’s vast resources and impressive economic potential.

With fiscal reform lowering taxes on inbound capital flow, a persistent removal of corruption and the dawning of a more conservative era, we are convinced that the Brazilian Real will become a more sought after, viable and lucrative diversification vehicle.